EN

In CNG v G & G [2024] HKCFI 575, in dismissing the application to set aside the arbitral award by CNG, the Honourable Madam Justice Mimmie Chan warned that the legal professional should be wary of making unmeritorious challenges to set aside arbitral awards by “massaging” cases to fall under the exceptional grounds of challenge under Section 81 of the Arbitration Ordinance (Cap. 609).

The Court once again reminded litigants that arbitration is a consensual process of final dispute resolution to which parties have voluntarily agreed to, and the limited recourse parties have under the Arbitration Ordinance is not intended to afford them with an opportunity to ask the Court after the event to go through the award with a “fine-tooth comb” to look for defects and imperfections under the guise that the tribunal failed to act within its remit.

Section 81 of the Arbitration Ordinance

With the consensual nature of arbitration and the tribunal’s autonomy at the heart of arbitral process, the grounds to set aside an arbitral award as compared to appealing a judgment in Court actions are much narrower. Before delving into the facts and issues of the case, it is helpful to note the permitted grounds to set aside a Hong Kong arbitral award under Section 81 of the Arbitration Ordinance:

In addition to the above, Schedule 2 of the Arbitration Ordinance contains opt-in provisions which provide for application to the Court to challenge an award on the ground of serious irregularity and for appeals to the Court on questions of law.

Given the limited grounds for challenge as set out above, in CNG v G & G, CNG attempted to find loopholes and problems in the award by “massaging” its challenges as “CNG was unable to present its case“, “the arbitral procedure was not in accordance with the parties’ agreement“, “the Award deals with a dispute not contemplated by or falling within the terms of the submission to arbitration“, and “the Award is in conflict with the public policy of Hong Kong” ([20]).

Facts and Issues

The dispute was between shareholders of a company (“SIL“) which own and operate a mining and processing project, whereby CNG, a state-owned enterprise of the PRC, owned 65% of the shares of SIL and the 1st Respondent owned the remaining 35% of the shares of SIL. Relying on the arbitration clauses contained in both the share purchase agreement and the shareholders’ agreement entered into between the two Respondents, CNG and SIL, the Respondents commenced arbitration proceedings at the HKIAC against CNG for the main claims that CNG (a) failed to honour a right of first refusal conferred on the 1st Respondent under the shareholders’ agreement in respect of CNG’s purported transfer of its shareholding in SIL (the “Share Transfer Claim“); and (b) failed to obtain the unanimous approval of the board of SIL before shutting down certain operations of the mining and processing project.

Failure to deal with issues / give reasons

The Respondents argued in the arbitration that as CNG had issued a valid transfer notice which met the requirements of the shareholder’s agreement to be an offer to the other shareholders, CNG was bound to sell the shares to the 1st Respondent as the only other shareholder of SIL. In contrast, CNG posited that the offer was an independent offer made to a permitted transferee (CGG, an affiliate of CNG by virtue of its control), and did not constitute a transfer notice within the meaning of the shareholder’s agreement which would afford the 1st Respondent the right of first refusal. The tribunal found that CNG’s transfer notice constituted an offer, which was capable of acceptance and was accepted, and that CNG was bound to sell the shares to the 1st Respondent in accordance with the shareholders’ agreement.

Before the Court of First Instance, CNG’s complaints placed reliance on the failure of the tribunal to deal with key issues or give reasons for its decision on the matter ([23]). For example, CNG emphasised that only 24 paragraphs of the total 163 paragraphs of the award were devoted to the tribunal’s reasoning for its decision on the Share Transfer Claim ([24]). Further, the tribunal did not deal with all the issues listed on the agreed list of issues submitted by the parties ([25]).

In response, Chan J noted that a long prolix judgment or award does not mean that it must contain sound reasoning or analysis of an issue or decision made. Vice versa, a short document likewise cannot indicate that there is no good reasoning or answer to the issue raised for decision ([24]). Moreover, an award is to be read and understood in the context of how the case was argued before the tribunal. In this case, it was logical for the tribunal to deal with the relevance of CGG being a permitted transferee under the shareholders’ agreement first. A decision in favour of the Respondents on this issue would render it unnecessary for the tribunal to determine whether, in fact, CGG was a permitted transferee ([33]). As noted by Chan J at [26]:

“…the tribunal does not have to set out each step by which it reaches its conclusion, and a failure to deal with an argument or a submission made on or relating to an issue is not equivalent to a failure to deal with an issue. The tribunal is not required to deal with each issue seriatim, as it can deal with a number of issues in the composite disposal of them. A tribunal does not fail to deal with an issue if it does not answer every question that qualifies as an issue. It can deal with an issue where that issue does not arise in view of the tribunal’s decision on the facts or its legal conclusions. A tribunal may deal with an issue by so deciding a logically anterior point such that the other issue does not arise. If the tribunal decides all those issues put to it that were essential to be dealt with for the tribunal to come fairly to its decision on the dispute, it will have dealt with all the issues. So long as a decision on one argument suffices to resolve an essential issue, the tribunal does not have to consider all arguments canvassed upon the issue. Although awards often respond to parties’ submissions, such submissions do not dictate how the tribunal is to structure the disposal of the dispute referred to it…a list of issues is not an exam paper, and I would add that it is not an exam paper with compulsory questions for the tribunal to answer them all.“

Further, the Court was not concerned with whether the tribunal had come to the right decision for the correct reasons, or whether there was evidence to support its finding in the decision ([31]). The Courts’ approach was to read an award generously with minimal curial intervention. Only when there are meaningful and readily apparent breaches of the rules of natural justice which can cause actual prejudice (rather than to comb an award in order to assign blame or to find fault in the process), may it warrant the setting aside of an award ([27]).

Procedural decisions and alleged inability to present case

In relation to procedure, it was argued for CNG that the tribunal had imposed an unequal and tight timetable on CNG, and had allowed the Respondents last-minute ambushes by adducing late evidence and running an unpleaded case, which resulted in CNG not being able to present its case ([22], [66]).

Citing COG v ES [2023] HKCFI 294, Chan J reiterated that a case management decision of a tribunal is not a decision which the Court should highly interfere with, in the absence of what the Court can find to be a serious denial of justice. Nor is it the function of the Court to descend to a level of reviewing the minutiae of the procedure, while the tribunal is obviously in the best position to decide on the most appropriate and fair manner of proceeding with the arbitration in accordance with the Arbitration Ordinance ([67]). For instance, as Section 46 of the Arbitration Ordinance provides a “reasonable opportunity” (as opposed to “full opportunity” used in Article 18 of the Model Law) to the parties to present their cases, no party can claim the right to have all the time it needs to prepare for the hearing and what the Court seeks to enforce is a standard of due process which are generally accepted as essential to a fair hearing ([68]).

Takeaways

CNG v G & G serves as another reminder from the Hong Kong Court that it does not sit on appeal against the tribunal’s finding of fact or law, nor interfere with the tribunal’s proper exercise of its case management powers. If parties attempt to rehearse once again before the Court arguments already made before the tribunal, or have different counsel reargue its case with a different focus in the hope that the Court may come to a different conclusion, it is likely to attract indemnity costs being awarded by the Court without changing the outcome of the case.

See full judgment here.

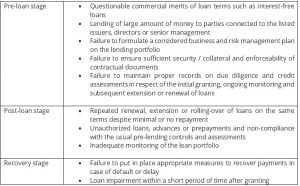

The Hong Kong regulators are taking actions in relation to their concerns regarding dubious loan transactions in listed companies. In mid-2023, the Securities and Futures Commission (SFC) and the Accounting and Financial Reporting Council (AFRC) published a joint statement on common regulatory concerns and provided guidance on conduct standards in relation to loans or other financial arrangements. In relation to misconduct of listed companies and directors, the April 2024 edition of the Enforcement Bulletin of the Hong Kong Stock Exchange (“HKEX“) discusses red flags commonly seen in lending arrangements of listed issuers and provides practical tips on compliance.

In recent years, the number of regulatory investigations involving loans, advances and other similar arrangements made by listed issuers has been on the rise. Some of the red flags below are often seen in various phases of the lending arrangements:-

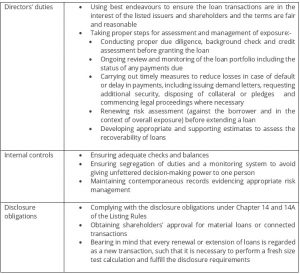

The Bulletin also provides practical tips on how to ensure compliance in respect of three areas which are the HKEX’s focus and major concerns, namely (i) directors’ duties, (ii) internal controls and (iii) disclosure obligations:-

The Bulletin serves as an important reminder of the HKEX’s rigorous oversight on loans, advances and other similar arrangements of listed companies. Listed companies and directors are advised to ensure that appropriate internal control measures are in place and the disclosure obligations under Chapters 14 and 14A of the Listing Rules are complied with. Directors should bear in mind their obligations under the Listing Rules, including a duty to safeguard the company’s assets, and they could be asked to demonstrate proper actions have been taken in accordance with established policies and procedures by producing relevant written records. Any material failure in safeguarding the assets of the listed company and/or giving due consideration regarding commercial rationale of proposed loan transactions will likely trigger regulatory investigations and enforcement actions.

In our February 2024 update, we discussed the proposed amendments to the 2018 Hong Kong International Arbitration Centre (“HKIAC“) Administered Arbitration Rules.

This article follows up on the launch of the 2024 version of the HKIAC Rules (the “2024 Rules“), which will take effect on 1 June 2024 (unless the parties have agreed otherwise) and incorporate most of the previously discussed amendments.

The 2024 HKIAC Rules is available here.

The key amendments are summarised as follows:

Overall, the 2024 revisions codify the HKIAC’s existing initiatives and clarify the powers of tribunals and the institution itself. These changes are a targeted enhancement which underscores the HKIAC’s commitment to maintaining its preeminent position in international arbitration.

In the recent case Manulife Financial Asia Limited v Kenneth Joseph Rappold & ors [2024] HKCFI 989, the Court of First Instance (“Court”) has once again emphasised the importance of ensuring that “non-compete covenants” (“NCCs”) in employment contracts are drafted in such a way that they go no further than reasonably necessary to protect the employer’s legitimate business interests.

Background

This decision concerns an application for interim-interim injunction against Mr Rappold (who was formerly employed by Manulife Financial Asia Limited (“Manulife“), the Plaintiff, as Chief Financial officer, Asia) from joining Prudential, which Manulife argued was its key competitor, pending determination of an interlocutory application.

Mr Rappold’s employment contract contained an NCC which provided, among other things, that for a period of 12 months following a voluntary termination of his employment, Mr Rappold must not be employed in a “Similar Capacity” by a “Competitor“[1].

The Court refused to grant an interim-interim injunction against Mr Rappold. In reaching this decision, whilst stressing that its views on the merits of Manulife’s claim should be treated as provisional in nature, the Court considered that (i) Manulife had not demonstrated that its claim to enforce the NCC had reasonably good prospect of success at trial; (ii) the balance of convenience was against the granting of such interim-interim relief.

No reasonably good prospect of success in demonstrating enforceability of NCC at trial

As a general principle, an NCC (being a form of restraint in trade) is prima facie unenforceable unless the employer can show that (i) it is reasonable in the interests of the parties and in the public interest, and (ii) it goes no wider than is reasonably necessary for the protection of the employer’s legitimate business interests.

There are three reasons contributing to the Court’s view that the NCC in this case may not be found enforceable at trial:

Balance of convenience lies against granting an interim-interim injunction

The Court was also of the view that the balance of convenience lies against granting an interim-interim injunction for the following reasons:

For the reasons above, the Court refused to grant an interim-interim injunction against Mr Rappold, which is the course that carries a “lower risk of injustice” in case the decision turns out to be wrong.

Takeaways

This decision serves as yet another reminder that an NCC should be drafted in such a way that the geographical scope and duration of the restraint is no more than necessary to protect the employer’s legitimate business interests. Any employer seeking injunctive relief should also be reminded to act swiftly and to prevent unnecessary delay.

Hence, when drafting an NCC, it is always helpful to first identify the legitimate business interests it seeks to address, such that a reasonable geographical scope and duration can be determined for the NCC. When the reasonableness of the scope is in doubt, it is equally helpful to use language which makes it easy for the relevant part to be severed out from the rest of the clause, such that the clause may be saved by the ‘blue pencil’ test.

The full decision can be accessed here.

[1] Both “Similar Capacity” and “Competitor” were defined in the NCC, and there was no dispute that by joining Prudential as Chief Transformation Officer, Mr Rappold was employed in a “Similar Capacity” by a “Competitor”.

[2] When a court is able to sever an offending part of the clause and leave the remaining part of the clause intact, it may do so and convert an otherwise unenforceable clause into an enforceable one. This is known as the ‘blue pencil’ test. The test requires: (i) that the severance must be carried out without adding or modifying the remaining wording; the remaining terms must continue to be supported by adequate consideration; and (iii) the removal of the severed words must not affect the meaning of the remaining part so as to change the character of the contract which the parties entered into.

On 23 April 2024, the Hong Kong Court of Appeal handed down two important decisions clarifying the applicability of the approach emerged from the Court of Final Appeal’s decision in Re Guy Kwok Hung Lam [2023] HKCFA 9 (“Re Guy Lam“) to disputed petition debts subject to an arbitration clause, and arbitrable cross-claims raised by a company in a winding up proceeding.

Re Simplicity – disputed debt subject to arbitration clause

In Re Simplicity & Vogue Retailing (HK) Co., Limited [2024] HKCA 299 (“Re Simplicity“), the Court of Appeal held that when the debt forming the petition debt is disputed and should be referred to arbitration pursuant to an arbitration agreement, the established approach, namely that a petitioner is ordinarily entitled to a winding order if the petition debt is not subject to a bona fide dispute does not apply. Rather, the approach in Re Guy Lam should apply, meaning the petitioner and the debtor company ought to be held to their contract to refer dispute to arbitration, absent countervailing factors such as the risk of insolvency affecting third parties, and a dispute that borders on the frivolous or abuse of process.

The controversy is whether the debtor company should be required to demonstrate a bona fide dispute of the petition debt on substantial grounds notwithstanding the existence of an arbitration clause in order for a petition to be stayed or dismissed ([33]). In this regard, the Court of Appeal held that it is appropriate such controversy should be laid to rest in light of the reasoning in Re Guy Lam, as the effect of arbitration clauses on insolvency petitions is of central importance to the reasoning of the Court of Appeal and Court of Final Appeal’s judgments of Re Guy Lam ([34]).

Further, having regard to the statutory framework protective of arbitration (as evidenced by Section 20 of the Arbitration Ordinance (Cap 609) which provides for the Court to refer matter subject to an arbitration agreement to arbitration), there is an even stronger case for upholding the parties’ contractual bargain that disputes falling within the scope of an arbitration clause should be resolved by arbitration ([37]). Vice versa, it would be an anomaly that a party bound by an agreement for dispute resolution cannot expect to proceed with an ordinary action for his claim, but can resort to the more draconian measure of presenting a petition for winding up a company ([35(5)]).

Importantly, such public policy consideration of holding parties to their bargain is not the only consideration and the approach of the Court in exercising its discretion is “multi-factorial” – the “countervailing factors” mentioned in Re Guy Lam, namely (i) the risk of insolvency affecting third parties, and (ii) a dispute that borders on the frivolous or abuse of process, are simply instances the Court may exercise its discretion not to hold the parties to their agreed dispute resolution mechanism. In this way, the Court retains the flexibility to deal with cases as circumstances require ([39]).

The Third Requirement of Lasmos survives

Prior to Re Guy Lam and Re Simplicity, the approach to disputed petition debt subject to arbitration clause is set out in Re Southwest Pacific Bauxite (HK) Limited [2018] HKCFI 426 as the “Lasmos” approach: the petition should generally be dismissed where it is shown that (i) if the company disputes the debt relied on by the petitioner, (ii) the contract under which the debt is alleged to arise contains an arbitration clause that covers any dispute relating to the debt, and (iii) the company takes the steps required under the arbitration clause to commence the contractually mandated disputed resolution process ([23]). In responding to the company’s submission in this case that the petitioner took no steps to express their intention to arbitrate, the Court of Appeal held that a genuine intention to arbitrate on part of the petitioner remains to be relevant. Otherwise, petitioners could simply raise arbitration clauses as a tactical move with no genuine intention to arbitrate in stalling the winding up process ([42]). However, even if no steps at all were taken, the Court could still exercise its discretion in appropriate cases to grant a short adjournment for the debtor to commence arbitration and require an undertaking from him to proceed with arbitration with all due dispatch. If no progress is made during the adjournment, the Court could consider lifting the stay and proceed to exercise its jurisdiction on the petition debt ([42]).

Nevertheless, as the company in this case did not file any evidence in opposition to the petition and did not comply with the condition for an extension of time to do so, the Court of Appeal dismissed the company’s appeal and ruled that the petitioner is entitled to a winding up order ([43]).

Re Shandong Chenming – The treatment of cross-claims

Further to our previous articles[1], the petitioner in Re Shandong Chenming Papers Holdings Limited [2024] HKCA 352 (“Re Shandong Chenming“) appealed the Court of First Instance’s stay of the petition to wind up the company pending determination of an arbitration between the parties. Following Re Simplicity, the principal question here is whether the approach in Re Guy Lam should also be applied where a company has raised a cross-claim against the petitioner which is arbitrated pursuant to an arbitration agreement between the parties. The petitioner submitted that the Court should assess the cross-claim in the ordinary case without an arbitration clause, the test being whether there is a genuine cross-claim based on substantial grounds.

To begin with, the petitioner submitted that there are two questions arising in a petition, the first being the threshold question of whether the petitioner has standing to present his petition. If the petitioner has standing, the second question is whether the company is insolvent and should be wound up. Within this framework, the petitioner posited that Re Guy Lam only concerned with the prior question of standing and the question of cross-claims falls under the second question, which is to be considered with a range of other matters in determining the insolvency of the company. Further, the petitioner argued that since the reason underlying the principle in Re Guy Lam is that the petitioner should be held to his bargain, that principle does not apply to cross-claim which is instead asserted by the company ([24]).

Contrary to the petitioner’s submissions, the Court of Appeal held that while it is true that the dispute over the petition debt is described in Re Guy Lam as a “threshold” question, it is relevant to note that the reasoning in that case is grounded in the wider context of the Court’s discretion to decline jurisdiction and it will be too narrow to read Re Guy Lam to confine its rationale to the question of standing to petition ([37]-[38]). Rather, the Court considers the overall relationship between the parties to see whether the petitioner is a net creditor having an interest to wind up the debtor company ([40], [42])). In this process the Court does not ignore the company’s cross-claims against the petitioner, and indeed regard them as “practically equivalent to disputes of the debt” where reverse cross-claims by the petitioner against the company could also be relevant ([39]). Therefore, where the cross-claim is subject to an arbitration clause, the forum agreement between the parties is likely to be relevant to the exercise of the Court’s discretion – for the Court to enter into the merits of the cross-claim would be against the parties’ agreement ([42]-[43]).

Moreover, the Court of Appeal held that while it is true that it will be the debtor company who has drawn the cross-claim to the Court’s attention, it is not the company seeking the Court’s determination of his cross-claim but the petitioner who is asking the Court to reject the cross-claim as a ground of opposition to the petition. For these reasons the petitioner is making a distinction without a difference and thus the appeal was dismissed ([45]).

Takeaways

The two Court of Appeal decisions put the controversy and debates sparked from First Instance’s decisions to rest and confirmed that Re Guy Lam applies equally to disputed petition debt and cross-claim subject to an arbitration clause.

Further, as the Court of Appeal made clear in Re Shandong Chenming, extending the Re Guy Lam approach to cross-claims would not create a “debt dodger’s charter” as the debtor company would have to show a valid exclusive forum agreement between the parties that governed the cross-claim to rely on the approach. In this light parties who have agreed to refer their disputes to arbitration should proceed with arbitration to resolve any issues before commencing winding up proceedings, so as to avoid wasted time and costs as the Courts will probably hold parties to their contractual bargain and stay or dismiss petitions, save for exceptional circumstances

[1] Articles published on 28 June 2022, 25 August 2023, and 15 November 2023

See news from our global offices